Is Amazon (AMZN) a Robotics Stock? 1 Million Robots and a Cash Flow Multiple Below Google's

TL;DR

Is Amazon a robotics stock? Yes. Amazon is the customer here, not the supplier. Every dollar the robots save stays inside its own margins.

- Amazon runs over 1 million robots. They touch roughly 75% of all customer orders. In 2020 the fleet was 200,000.

- It owns Zoox (self-driving, $1.2B in 2020). It is testing the Digit humanoid in live warehouses. In March 2026 it acquired Fauna Robotics, a home-humanoid startup.

- Vulcan is its first robot with a sense of touch. It already picks and stows roughly 75% of everything Amazon stores.

- Retail margin is 5.83%. Add 1 to 3 points on $588 billion of retail revenue and you get billions in new operating income every year.

- Amazon trades at 17.24x price to operating cash flow. Google trades at 24.82x. The P/E says the opposite, because reinvestment suppresses the earnings line and not the cash.

- The main risk is CapEx. $130 billion in 2025, a projected $200 billion in 2026. The real danger is data centers arriving late because of power or permitting.

Is Amazon a robotics company, or a retailer that happens to use robots?

Both. That is what makes it hard to value. Amazon does not sell a single robot to anyone. There is no robotics revenue line to model. There is no segment to compare against competitors. The entire return shows up as cost that never gets spent, and that lands in the operating margin. They've chosen to scale through vertical integration and it seems to be working pretty well.

Why did Amazon buy Kiva Systems?

Amazon paid $775 million for Kiva Systems in 2012. The reason was simple. Between 50 and 60% of warehouse labor costs came from workers walking to find inventory.

Kiva flipped that. Its robots carried entire shelving units to the workers, instead of sending workers to the shelves.

Deutsche Bank estimated the result. Within four years, operating expenses fell by roughly 20% per warehouse. That is about $22 million saved per fulfillment center. The $775 million deal became the blueprint for everything after it.

How many robots does Amazon have?

Amazon had 200,000 robots in 2020. Today it has over a million. The fleet handles roughly 75% of all customer orders at some point in the journey.

Amazon is not building all of this in-house. In 2022 it committed $1 billion to the Amazon Industrial Innovation Fund. The fund invests exclusively in robotics and automation companies. It has since expanded into last-mile delivery and autonomous vehicles, and it has backed 26 companies so far.

Can Amazon's robots replace warehouse workers?

Not with the current fleet. Today's robots handle structured, predictable tasks. But the moment an item is fragile, irregular, or packed strangely, a human hand takes over. That gap is the practical ceiling of warehouse automation. It is also what the fund was built to attack.

Agility Robotics was one of the fund's first investments. The company builds Digit, a humanoid robot that Amazon is now testing in its own warehouses. Digit walks upright, navigates around obstacles, and works in buildings designed for humans.

That last part carries the weight. Amazon has more than 1,300 active logistics facilities globally. A robot that works in the existing ones, without redesigning a single building, changes the deployment math.

In March 2026 Amazon went further and acquired Fauna Robotics. Fauna builds Sprout, a 42-inch humanoid that walks, opens doors, recognizes its name, and handles small household tasks. It runs on NVIDIA's Jetson Orin platform. Fauna now sits inside Amazon's Personal Robotics Group.

Keep in mind Sprout is a home robot, not a warehouse one. It seems Amazon wants to start selling humanoids.

What is Amazon's Vulcan robot?

Vulcan is Amazon's first robot engineered with a physical sense of touch. It can feel how hard it is gripping or pushing. That lets it handle items it was never specifically trained on.

Vulcan already picks and stows roughly 75% of everything Amazon stores in its fulfillment centers. It works at speeds comparable to a human. And when it cannot safely move an item, it asks a human to step in instead of forcing it.

Digit solved movement. Vulcan is the answer to the other half. Most robots cannot feel what they are holding, which is why fragile items have always gone to a human hand.

Why did Amazon buy Zoox?

Amazon acquired Zoox in 2020 for $1.2 billion. On the surface it looks like a side bet, since self-driving cars and online retail have nothing to do with each other.

But Zoox is not really a robotaxi company. It is a self-driving technology company that happens to be selling rides right now.

Zoox has given more than 500,000 free rides across Las Vegas, San Francisco, Austin, and Miami. Waymo does 500,000 paid rides every single week, and it is expanding into Europe and Asia. The two are at completely different stages. Zoox is years behind on commercial scale.

The connection to Amazon's core business is the technology. Zoox generates real-world driving data at scale. That same stack becomes the foundation for autonomous last-mile delivery. The vehicle carrying passengers today runs on the platform that carries packages later.

Can Amazon deliver packages without drivers?

Last-mile delivery accounts for up to 53% of total shipping cost. Most of that is labor.

So picture the endgame. A self-driving vehicle stops in front of your home. A robot steps out and walks the package to your door. That takes out the single largest cost in the delivery chain.

The drone program runs on the same logic. Prime Air is targeting 500 million deliveries by 2030. Right now a drone delivery costs Amazon around $63, while the customer pays about $10. That gap looks terrible in isolation, but it shrinks once the fleet is built and the infrastructure is paid for. After that, each extra delivery costs a few cents in electricity. The expensive part is building it.

How much does Amazon save with robots?

At today's scale you have to size the savings through the margin instead.

Amazon's retail margin is 5.83%. That figure already includes high-margin advertising revenue, so the pure retail and logistics operation runs lower.

Now do the math. Robots adding 1 to 3 percentage points on $588 billion in retail revenue means billions in new operating income every year.

Amazon's internal documents project it can double sales volume without hiring an additional 600,000 workers. Long story short, the cost base stays flat while the revenue base doubles.

Is Amazon's business growing in 2026?

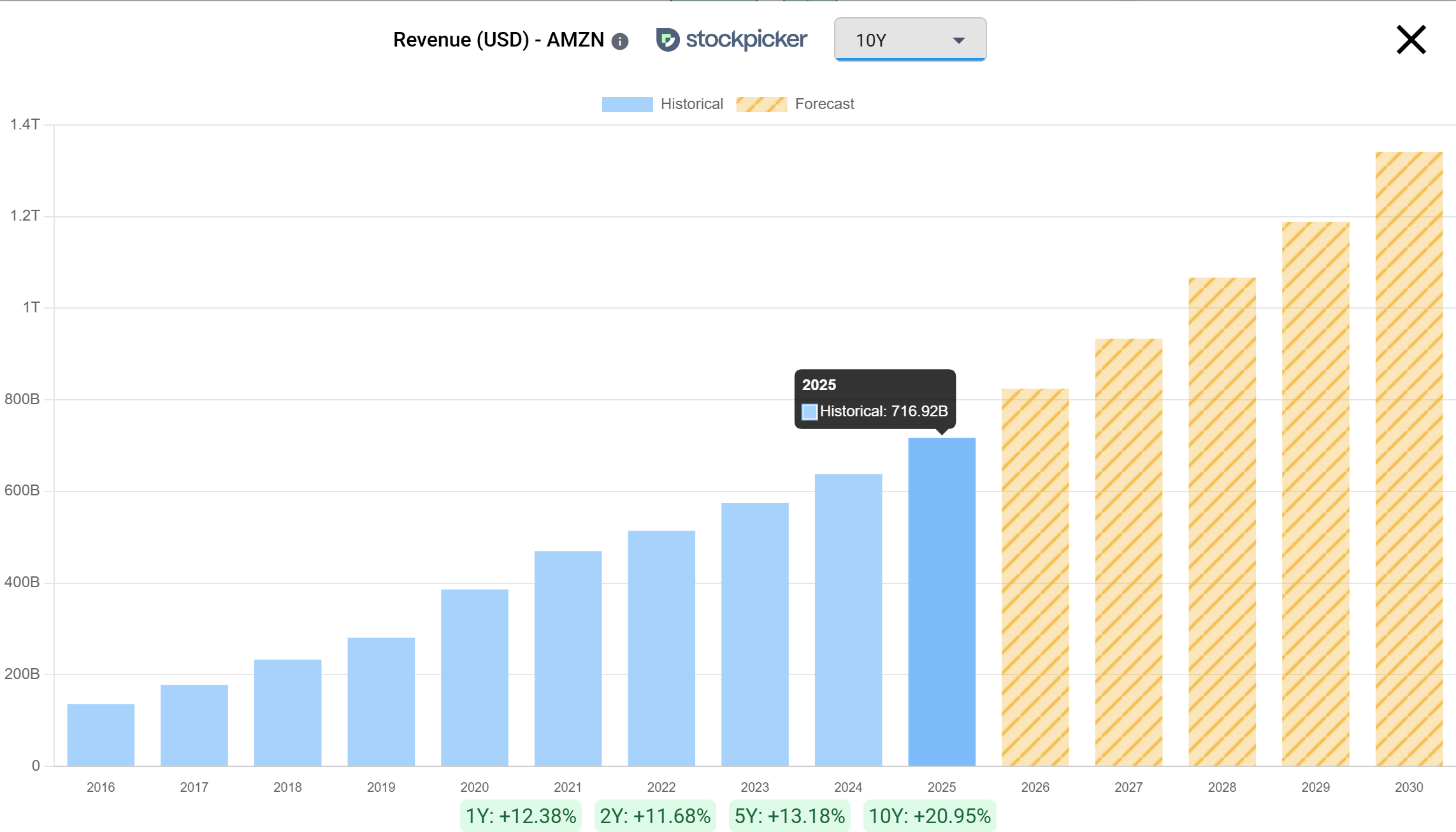

Yes, and it is accelerating. Revenue for 2025 was $716 billion. That makes Amazon the company with the highest revenue on earth.

Analysts project $824 billion for 2026. That is 15% growth, an acceleration from last year's 12.4%. The 2030 forecast comes in at $1.34 trillion.

Check AMZN fundamentals

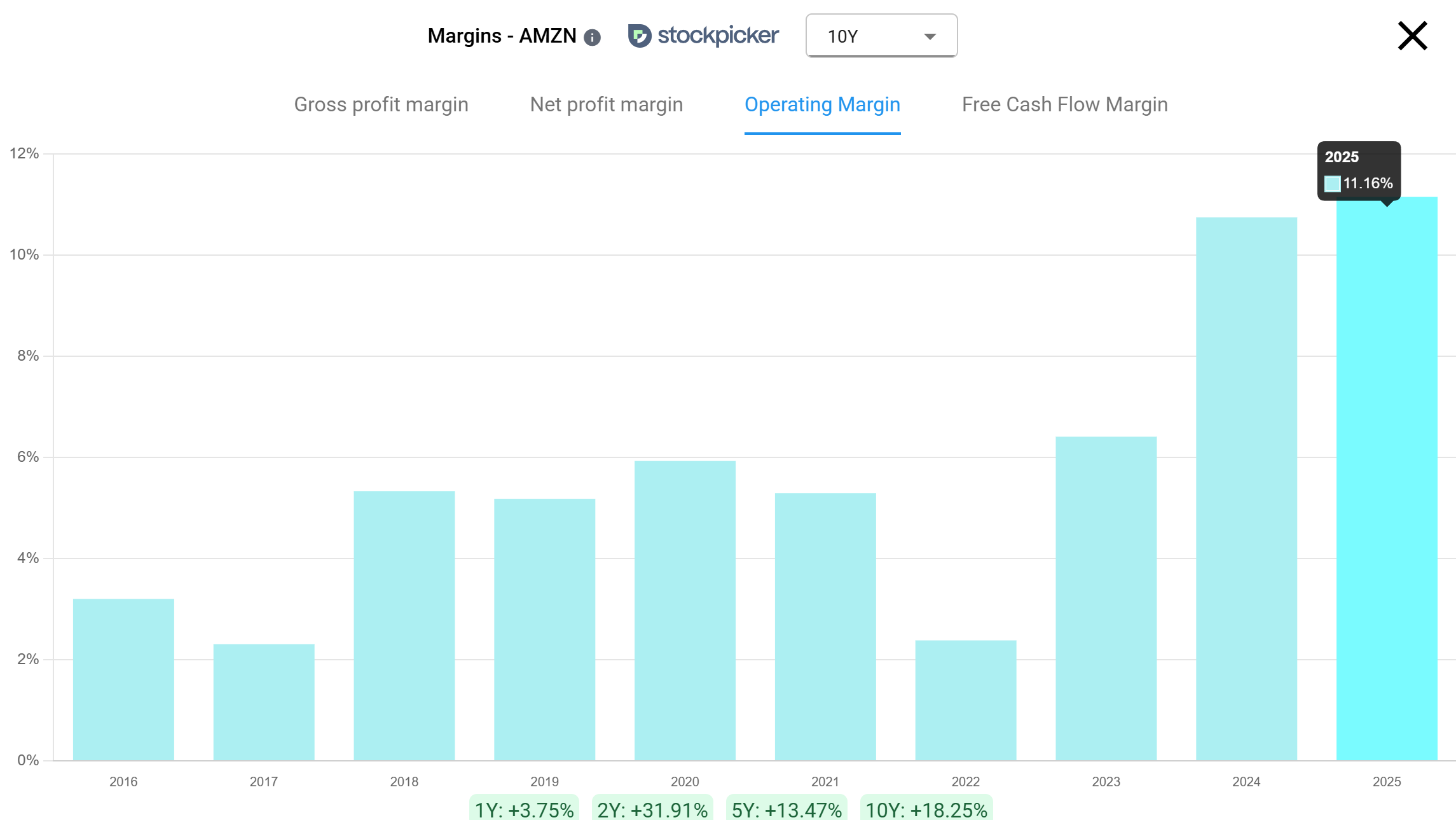

Operating margin went from 6.4% in 2023 to 11.16% in 2025. The main driver is AWS growing faster than retail, and AWS margin last quarter was 37.6%. In Q1 2026 the operating margin hit a record 13.1%.

[Chart: AMZN operating margin 2023-2026] Alt text: Amazon operating margin chart 2023 to 2025

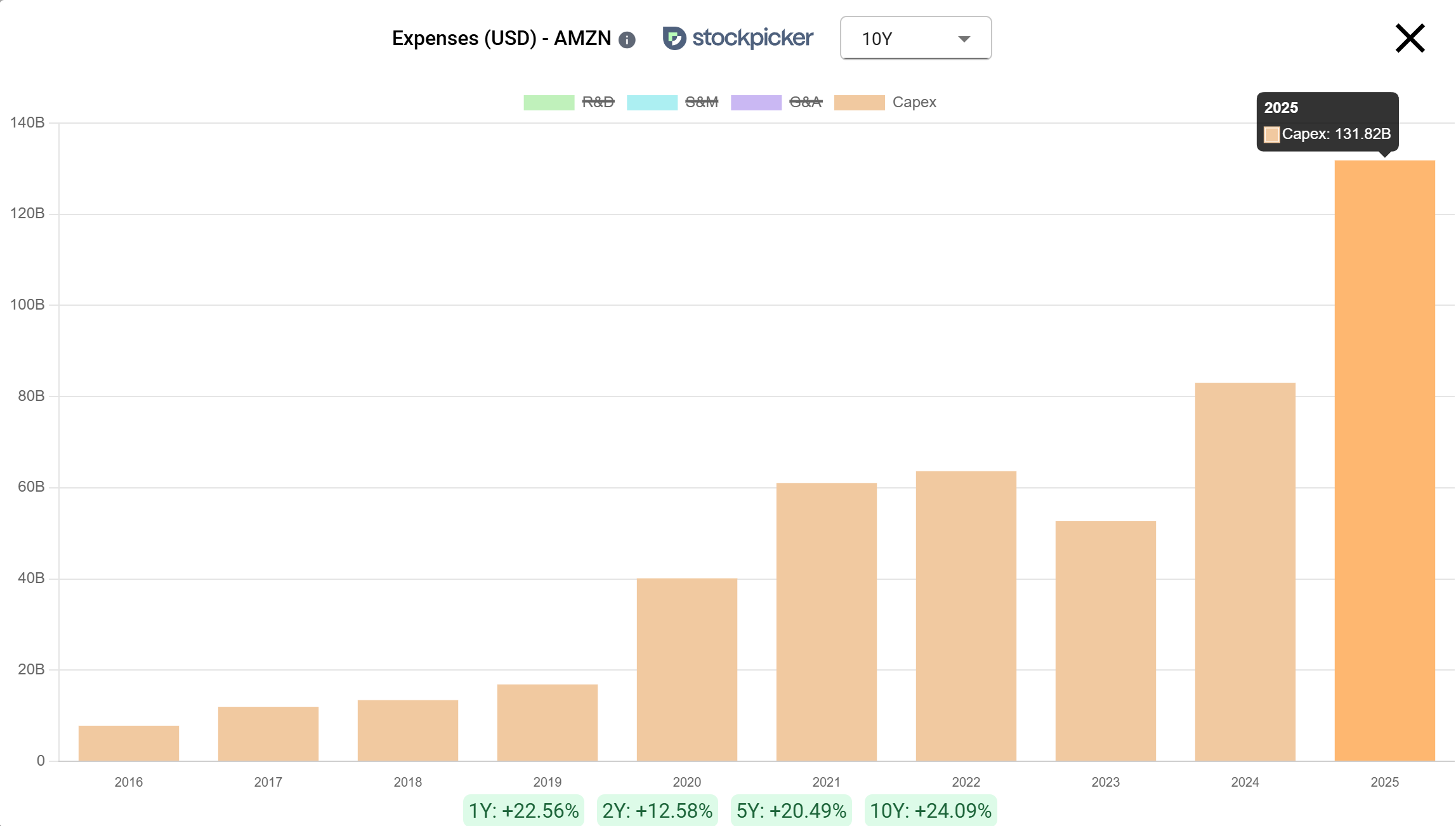

What is Amazon's CapEx for 2026?

CapEx was $130 billion in 2025. It is projected at $200 billion for 2026.

Amazon's retail business is capital intensive by definition. The cloud business is capital intensive too, and that is what drives the number up. CEO Andy Jassy keeps saying the same thing: they do not have enough capacity to meet cloud demand. Whenever they build new capacity, it gets sold. The same pattern is showing up across every hyperscaler

The bigger risk is not the CapEx itself. It is data center delays from power shortages or regulatory approvals. That would mean the money is spent and the revenue arrives late.

Why Amazon's P/E ratio is misleading

Amazon's P/E looks expensive because reinvestment suppresses net income. Not because the business is priced richly.

Amazon has reinvested every dollar since the beginning. Even now, at a $2.5 trillion valuation, it keeps reinvesting heavily. That keeps reported profit and free cash flow low.

Price to operating cash flow is the better metric here. In plain language, operating cash flow is the money the business brings in from running itself, before Amazon spends it on warehouses, robots, and data centers.

On P/E, Amazon has looked overvalued for most of its life. On cash flow, it has not.

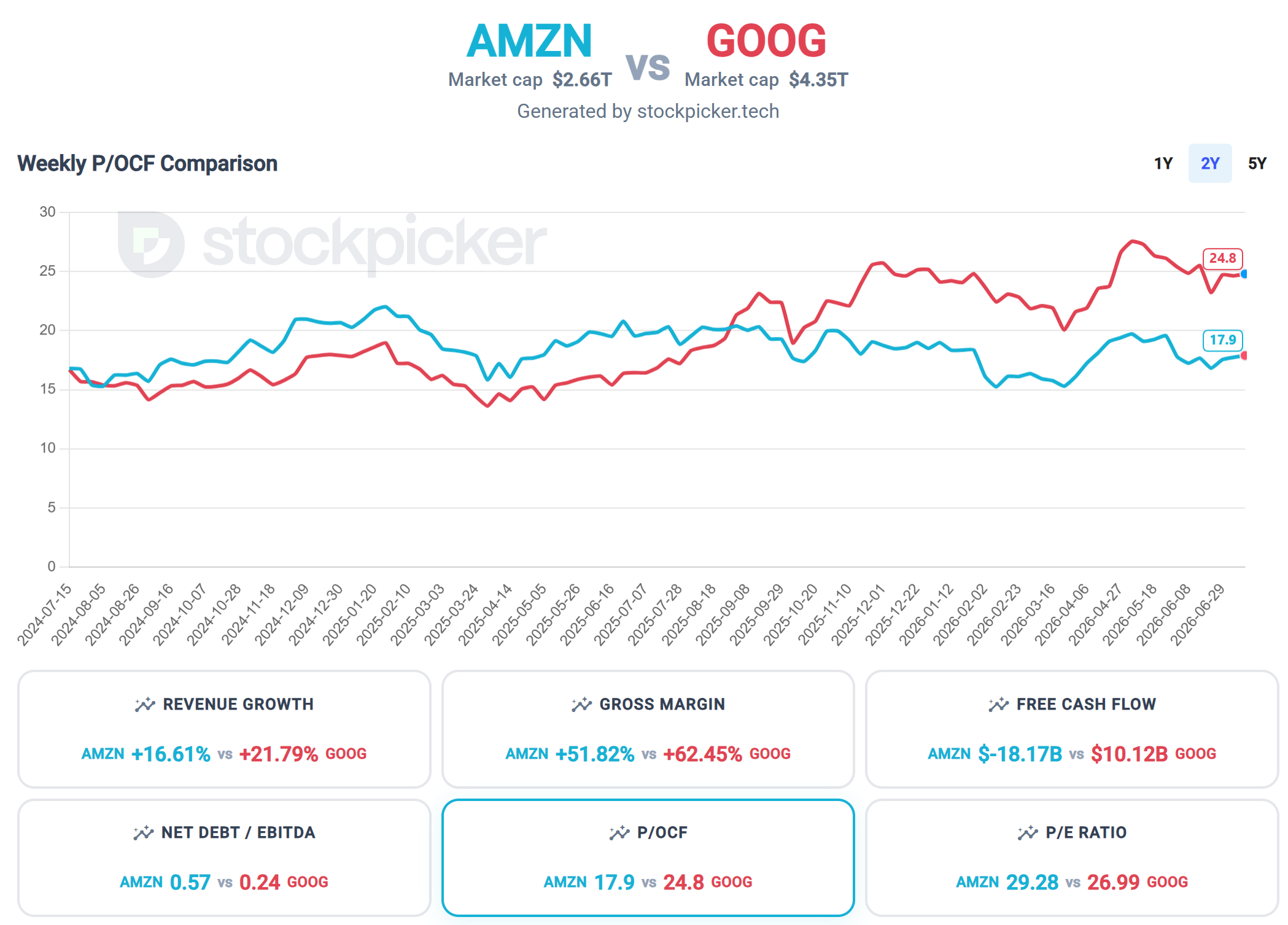

Is Amazon cheaper than Google?

I ran AMZN and GOOGL through the Stockpicker Comparison Tool.

On P/E, investors are paying almost 50% more for Amazon than for Google. Switch to price to operating cash flow and the ranking flips. Google trades at 24.82. Amazon trades at 17.24.

The reason for the gap is the spending. It suppresses Amazon's earnings line while the cash generation underneath keeps growing. Same company, two metrics, two completely different stories.

Compare up to 4 stocks with Stockpicker Comparison Tool

Is Amazon stock undervalued in 2026?

On price to operating cash flow, Amazon trades below Google while growing faster.

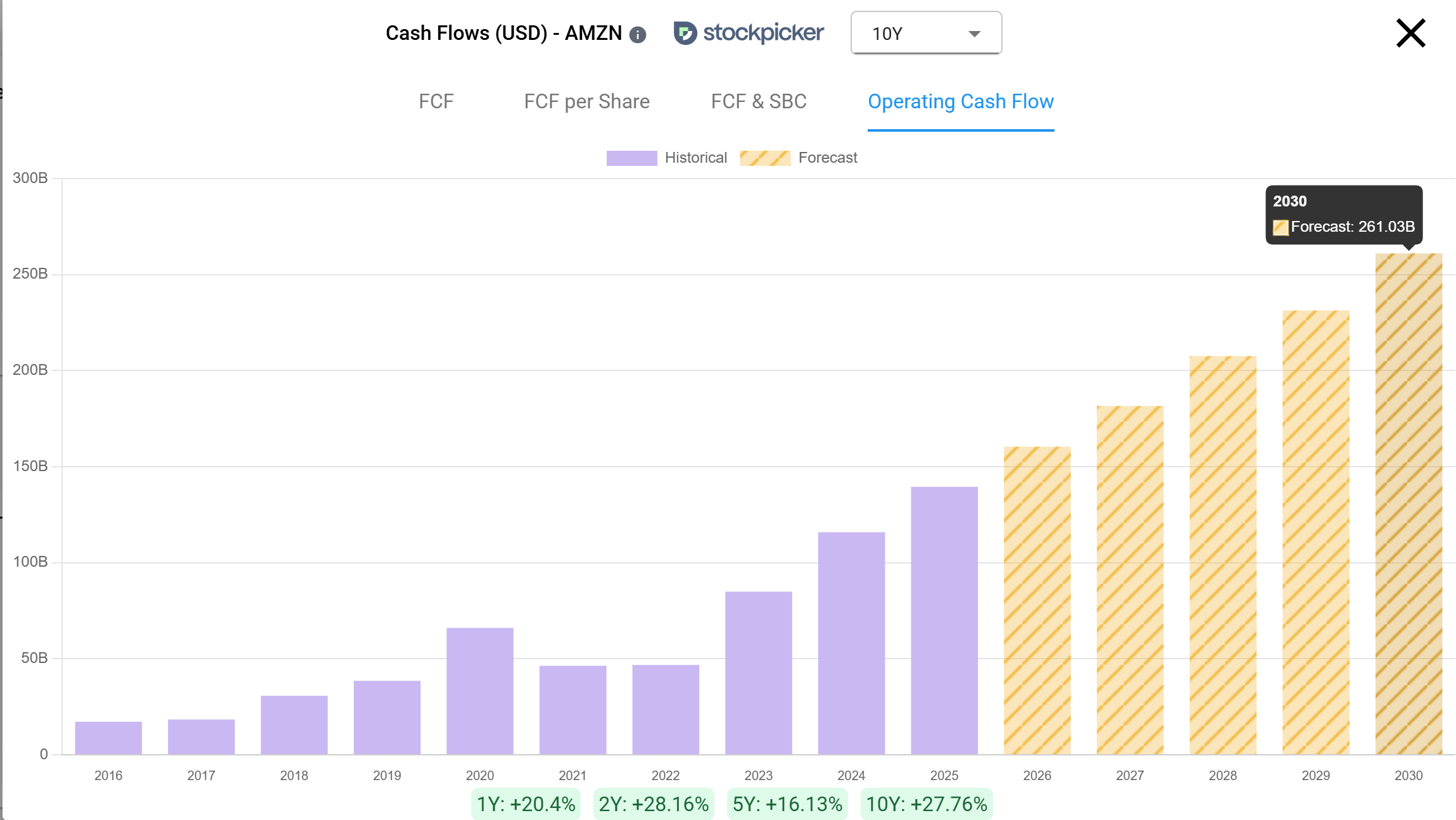

Analysts project operating cash flow almost doubling by 2030, from $139 billion to $261 billion. Apply a 15 to 20x multiple to that. You land somewhere between $4 and $5 trillion in market cap.

Keep in mind a lot can happen in five years, in either direction. The bear case is straightforward. CapEx keeps climbing. AWS capacity arrives late because of power or permitting. The humanoid programs stay in pilot phase for another decade. And the margin expansion never shows up.

Where I land

Amazon builds the robots. The software making them intelligent is being built somewhere else, at NVIDIA, which I cover separately ([link to NVIDIA post]).

But on the question this post started with, I think the answer is yes. Amazon is a robotics stock. The robotics program is a real part of the operating margin story, not a side project.

Full disclosure: I own Amazon stock. It is my second-largest holding across my two portfolios. I was buying throughout 2025 and have not added in 2026. Do your own research before making any decisions.

If you want to see how Stockpicker compares to other tools, I broke down the best stock research websites in 2026.

Not financial advice. I am not a licensed financial advisor. Everything above is personal research and opinion.