Hyperscaler CapEx Is the Only Metric That Matters Right Now

TL;DR:

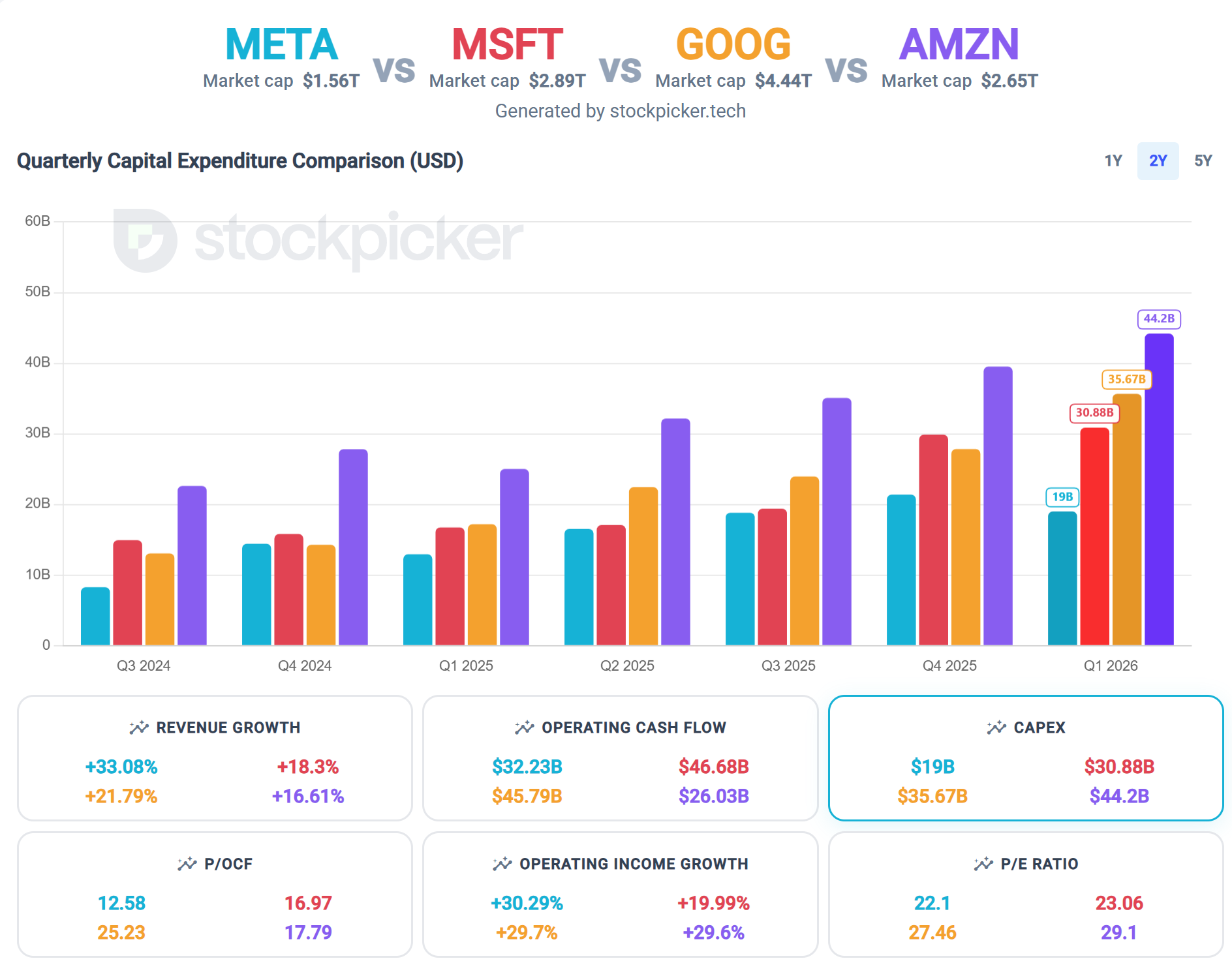

- The four largest hyperscalers are set to spend roughly $725 billion on capex in 2026: Amazon $200B, Microsoft $190B, Alphabet $180-190B, and Meta $125-145B.

- This spending is holding up a K-shaped market. AI infrastructure stocks are surging while other industries, like software and financials, have dropped YTD.

- Operating cash flow is not keeping pace. Alphabet raised $80 billion in equity for the first time since its IPO, and Amazon is taking on more debt to fund the gap.

- Much of the CapEx is a hedge against Nvidia, funding custom chips (Google's TPU v7, Microsoft's Maia 200, Amazon's Trainium 3) to cut costs by 50% or more.

- Power is now the real bottleneck, not chips. Morgan Stanley estimates 34 gigawatts of new capacity by 2027, enough to power 15 million US homes.

- The main risk is a monetization lag. AI software revenue is running 12-18 months behind the spending, and short 3-5 year depreciation schedules will pressure margins if it doesn't catch up.

The S&P 500 is up only 9% year-to-date, while AI infrastructure stocks like MRVL, CRDO, AMAT, and ASML have surged. This is a K-shaped market where one part is thriving and the rest is barely moving, and hyperscaler capex is the reason for the divide.

Analysts are speculating that AI infrastructure spending could hit $1 trillion by 2027, which makes it the single most important number for both the index and the broader economy right now. The problem is that hyperscaler operating cash flow is not growing fast enough to match the spending. If that gap does not close, capex will have to come down, and that would hit the entire AI supply chain.

Here is how each of the four majors is handling the pressure.

Alphabet (GOOG) CapEx: $80B in New Equity

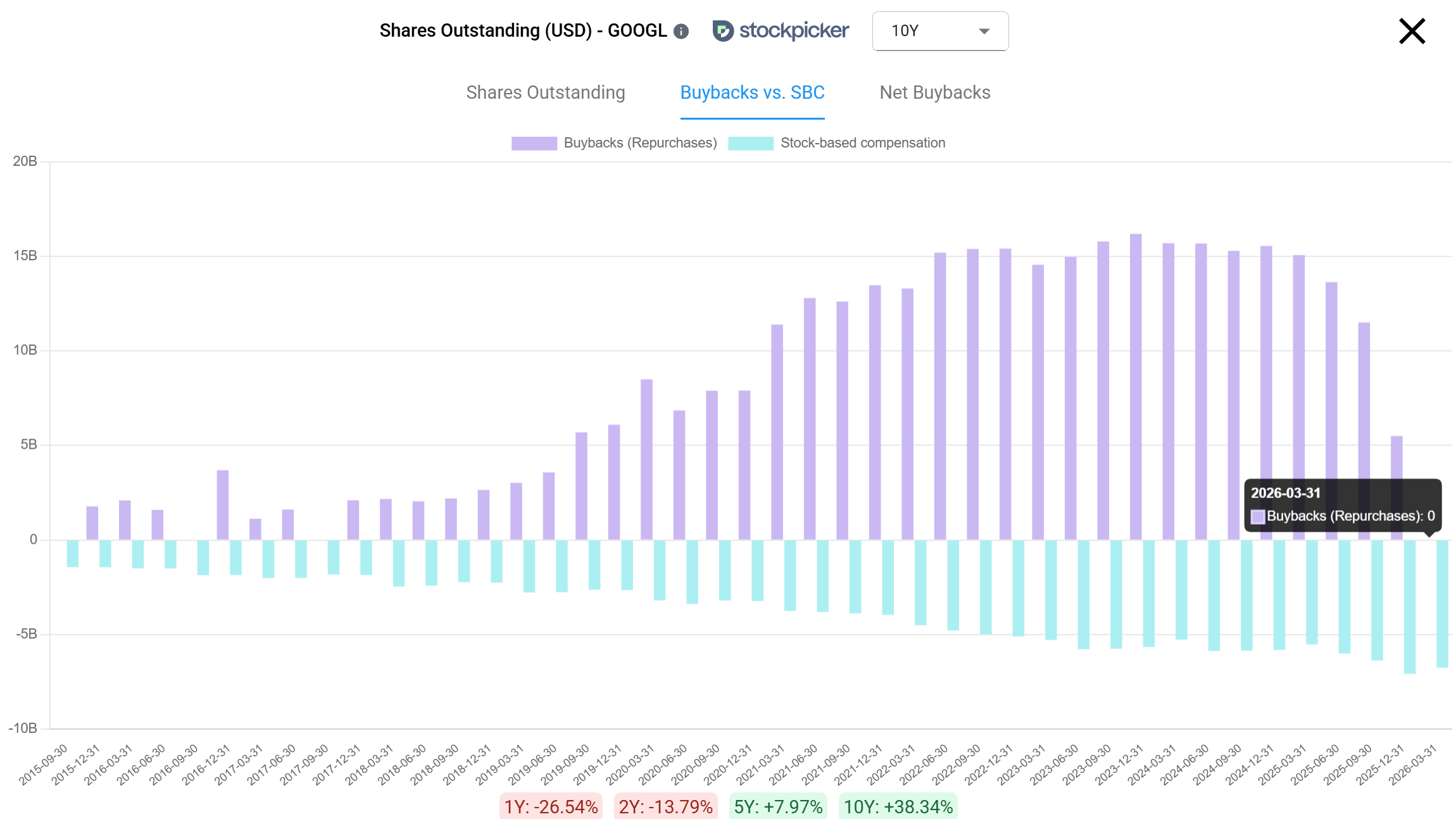

Alphabet did something it has not done since its IPO: it raised $80 billion in equity and took on more debt to help fund AI infrastructure. Google has historically been an aggressive buyer of its own stock, not an issuer of new shares, so this is a real signal. Last quarter GOOG stopped their share buyback program.

Alphabet is currently the strongest-performing hyperscaler, driven by tight integration between Gemini and Google Cloud, and its core search business is capital-light. Even so, the company committed to $180-190 billion in capex for 2026, and that number is large enough that even Alphabet's cash flow could not cover it without raising outside capital. When Google needs to raise money, that tells you how heavy this spending cycle is.

Amazon (AMZN) CapEx: $200B and More Debt

Amazon's capex for 2026 is set at $200 billion. CEO Andy Jassy keeps saying AWS is sold out and they cannot build fast enough to meet demand.

The reason Amazon is willing to spend this much is AWS itself. AWS is only about 18% of Amazon's revenue, but it brings in more than half of the company's operating income, and it runs at operating margins above 35%. It is the profit engine paying for the whole AI transition, so management is chasing that profitable cloud revenue as hard as it can.

Unlike Google, Amazon's core retail business already uses a lot of cash on its own. Operating cash flow has grown a lot, mostly because of AWS, but it is still not enough to cover the front-loaded spending.

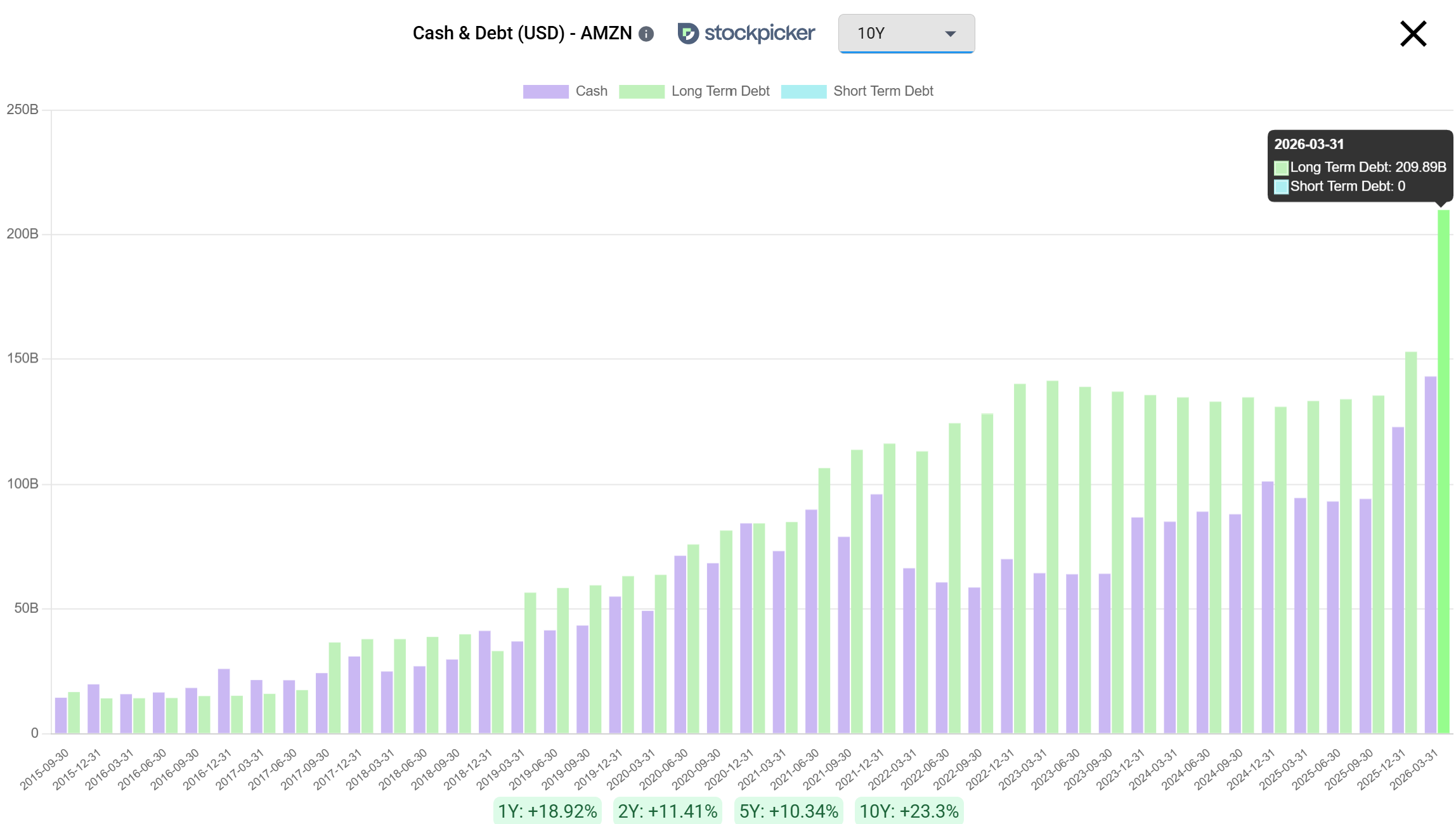

So Amazon is turning to the debt markets. After raising around $54 billion in bonds earlier this year, they came back in July with another $25 billion sale and told their bankers that would be the last one for 2026.

You can see this show up directly on the balance sheet. Amazon's long-term debt jumped to $209.89 billion in Q1 2026, up from around $153 billion the quarter before. That is roughly $57 billion of new debt in a single quarter.

I would not read this as a warning sign. Amazon is using cheap debt to fund assets that earn high returns, instead of issuing new shares and diluting existing owners. The trade-off is that all this spending pushes free cash flow down in the near term, in exchange for locking in cloud customers for years. That is a trade Amazon is clearly happy to make.

Microsoft (MSFT) CapEx: The ROIC Drag

Microsoft's capex for 2026 is projected at $190 billion. Microsoft was the undisputed AI leader three years ago, but sentiment has since turned negative and the stock is down roughly 19% year-to-date in 2026.

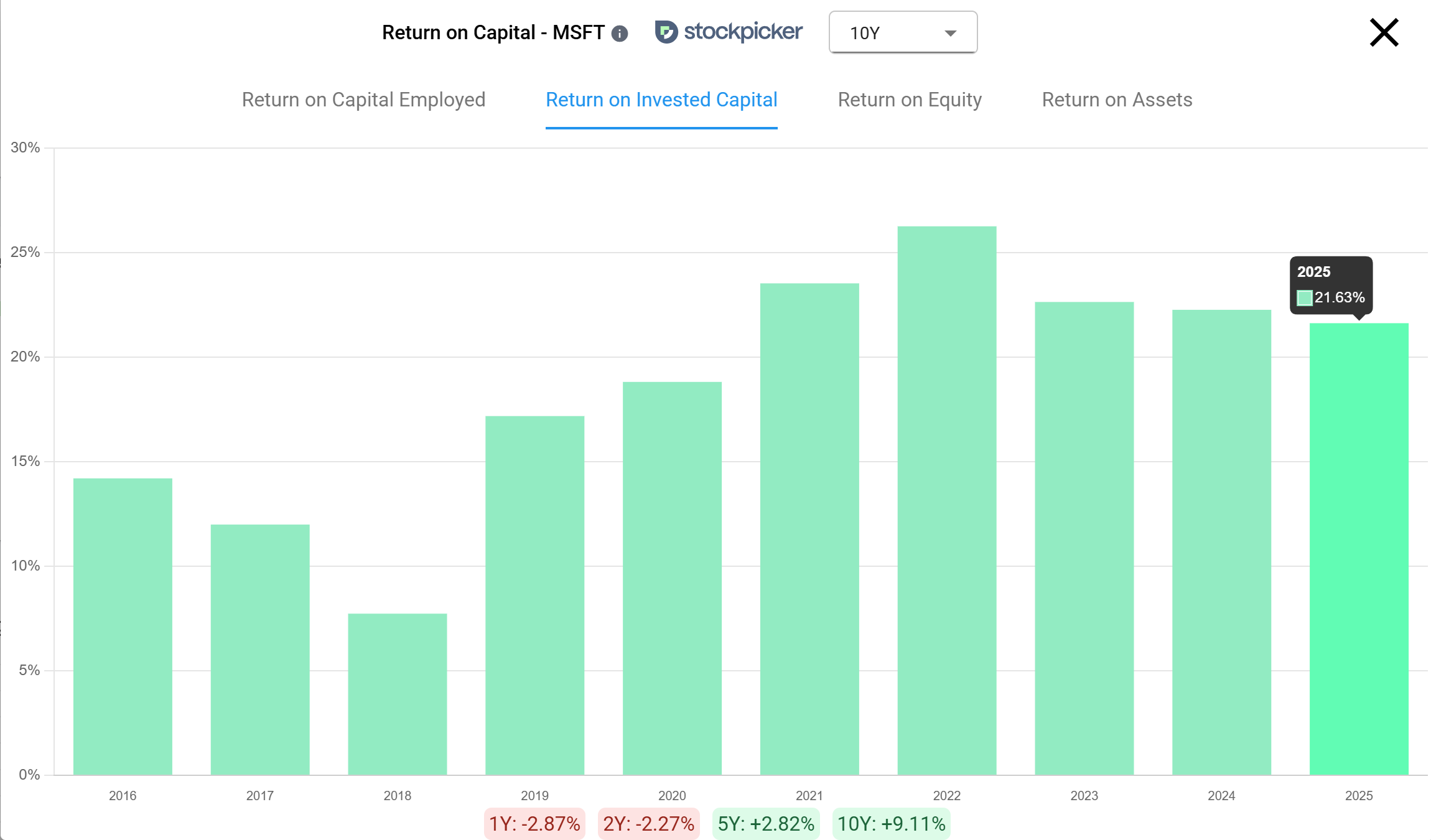

Despite that, Microsoft is still the largest cash generator of the four. To fund the $190 billion, they are cutting costs elsewhere and tapping debt markets. Adding hundreds of billions to invested capital guarantees a near-term drag on return on invested capital (ROIC), no matter how well the underlying business performs. ROIC for 2025 was 21.63%, and the new spending will pull that number down before it pays off.

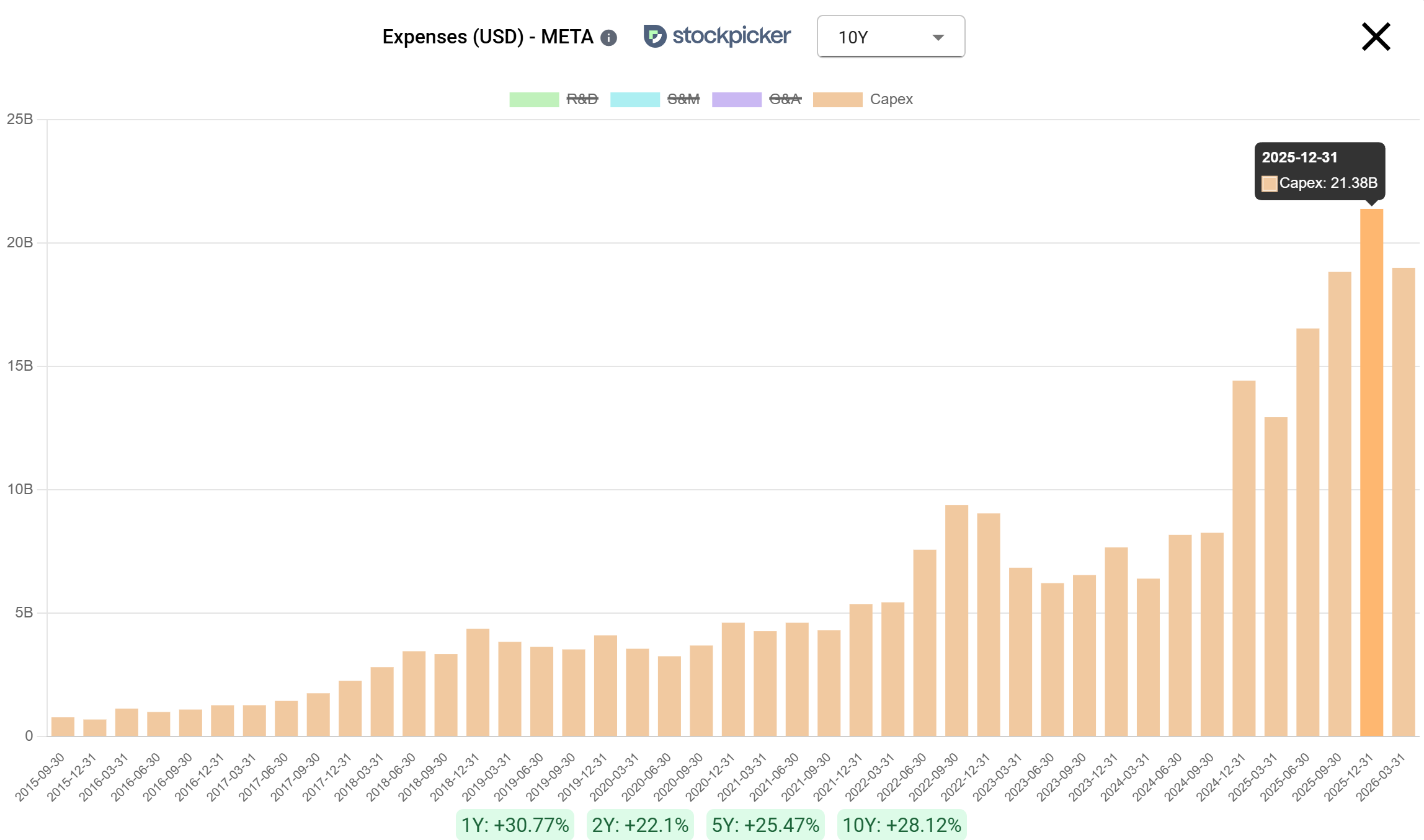

Meta (META) CapEx: Funding It With Meta Compute

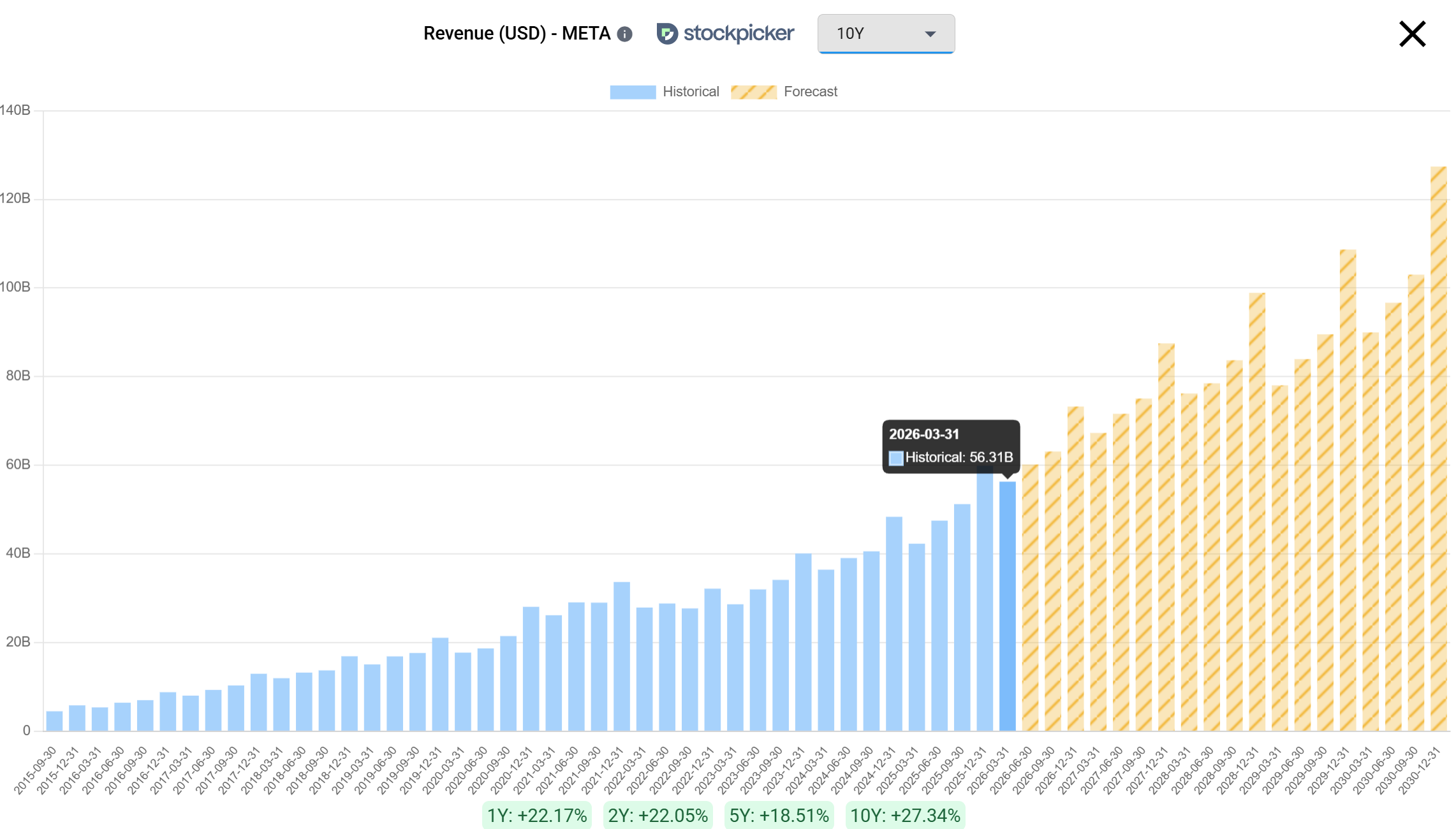

Meta posted the highest revenue growth of the group last quarter at 33%. That number is already a sign the AI spending is working, because most of those gains come from better ad targeting running on the same infrastructure. Even so, the stock spent most of the year down, because investors were nervous about the sheer size of the $125-145 billion Meta planned to spend and wanted to see it turn into a more direct return.

That is what changed with Meta Compute. Meta is entering the cloud business by renting out the computing power it is not using itself, and when the news broke the stock jumped 9% in a single day, its best day in months. Selling the spare capacity turns part of that spending into revenue right away, instead of waiting on consumer AI products that are harder to predict. Meta is the only one of the four without an existing cloud business, so this is a logical way to make money on infrastructure it was building anyway.

Where the $725B Is Actually Going

Custom Silicon and the Nvidia Question

A large part of hyperscaler capex, and nobody knows exactly how much, is really a hedge against Nvidia's pricing power. Every major hyperscaler is pouring money into its own chips (ASICs) to run inference more cheaply.

A rising portion of Alphabet's $180-190 billion capex is funding TPU v7 production. Microsoft's $190 billion covers the rollout of custom Maia 200 chips built for OpenAI's models. Amazon is scaling up Trainium 3 silicon for the same reason, to avoid waiting on Nvidia's lead times. The goal across all three is the same: cut chip costs by 50% or more and depend less on Nvidia over time.

The Power Grid Bottleneck

You cannot deploy hundreds of billions in infrastructure if you cannot plug it into a wall. Physical land and power grid access are becoming more expensive than the computing hardware itself. Morgan Stanley estimates the four companies combined will add up to 34 gigawatts of compute capacity by 2027, which is enough to power roughly 15 million US homes.

This is where Meta's $125-145 billion capex is misleading if you assume it is mostly GPU clusters for training Llama. A large part of it is going into power shells, land, and liquid cooling infrastructure that will not come online until 2027 or later. They have sign contracts with Vistra corp., Oklo and other companies to secure the power they need. The power grid, not the chips, is becoming the real bottleneck of this cycle.

The Monetization Lag

Hardware and data center assets are being front-loaded on the balance sheets today. The software that is supposed to justify all of it, things like corporate Copilots, Gemini Advanced, and enterprise AI workflows, is running 12 to 18 months behind in actual cash generation.

These assets depreciate over short 3 to 5 year windows, so the depreciation is going to weigh on operating margins over the next few quarters no matter what. Software revenue needs to catch up fast enough to justify the spending before that pressure shows up in the numbers.

What Happens If Hyperscaler CapEx Slows Down

This entire AI supply chain depends on Big Tech continuing to spend at this pace. If application revenue does not pick up soon, these four companies will be forced to pull back on capex, and the K-shaped market will lose the one thing holding it up.

It is important to understand that companies like Micron and Sandisk have been going up in price mainly because hyperscalers need their products, so they(as well as other AI bottleneck companies) are highly sensitive on hyperscaler CapEx.

You can compare all four companies' operating cash flow and free cash flow trends side by side using the Stockpicker Comparison Tool, or check the individual fundamentals for Alphabet (GOOG), Amazon (AMZN), Microsoft (MSFT), and Meta (META).

Full disclosure: I own shares of GOOG, AMZN, META and MSFT.

This post is for information purposes only, it is not financial advice. Do your own research.

See our breakdown of CRDO's 1.6T optical transition risk

If you are evaluating research tools more broadly, our roundup of the best investment research websites in 2026 is a good place to start.