CRDO Stock: Will the 1.6T Optical Transition Destroy Credo's AEC Moat?

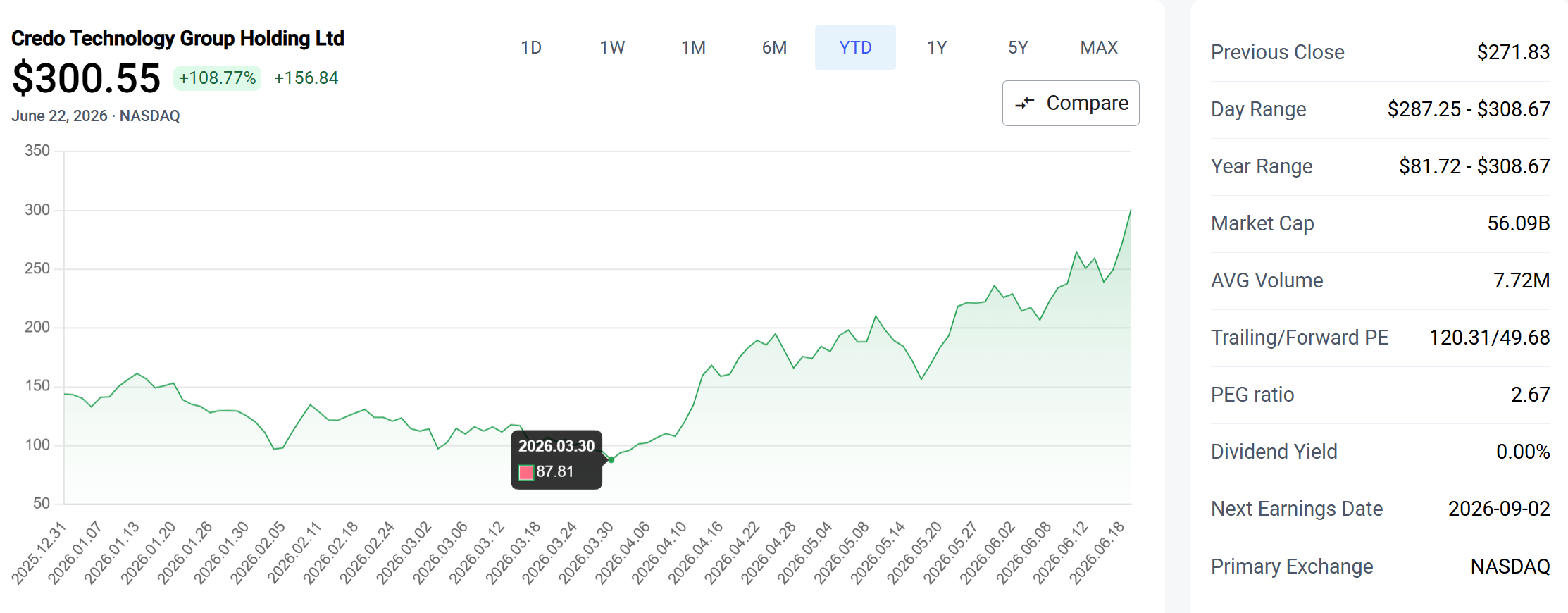

A one-millisecond connection glitch inside an AI data center can instantly cost millions of dollars. Credo Technology built the solution to that problem — and the market noticed. The stock is up 300% in two months and today it finally surpassed $300 per share.

Here is whether the fundamentals justify it.

CRDO Fundamental Analysis Fast Facts:

- Core Product: Active Electrical Cables (AEC) with 50% lower energy use than optical alternatives.

- Growth Metrics: +157% YoY revenue growth ($437M last quarter); 68% gross margin.

- The Core Risk: The industry transition from 800G to 1.6T speeds where copper hits physical limits.

- Valuation: Hyper-growth is real, but priced at an aggressive 34x Price-to-Sales (P/S) ratio.

Credo Technology (CRDO) Active Electrical Cable (AEC) Architecture

Credo Technology Group (CRDO) provides AI connectivity solutions. In plain language: cables.

They developed the Active Electrical Cable (AEC), which has become the industry standard for short-range connectivity inside data centers. To understand why, you need to understand the architecture.

An AI data center consists of tens of thousands of chips grouped in server racks. Those chips must be connected. When it comes to data center cabling, two things matter most: energy consumption and connection stability.

If there is a link flap — a short interruption in the connection — the entire AI training process can crash. Hyperscalers lose millions of dollars instantly.

Credo's cables solve both problems at the same time. They consume 50% less energy than optical alternatives, and their zero flap technology improves connection reliability 1,000 times compared to competitors.

CRDO Competitive Advantage: PILOT Platform & Switching Costs

Credo's competitive advantage comes from three things.

First mover advantage: Their R&D team is years ahead of the competition. Their processing chips use mixed-signal architecture, which cuts manufacturing costs while lowering risk for hyperscalers.

PILOT platform: This is Credo's proprietary software platform, already deeply embedded in customer workflows. PILOT runs continuous zero-flap checks, stopping potential interruptions before they happen. This creates switching costs that go far beyond the cables themselves.

Switching cables in a multibillion-dollar data center is not like unplugging an HDMI cable. These server racks are engineered from day one around Credo's specific cable design. Once a hyperscaler builds around Credo, leaving is incredibly painful.

Patent wall: Credo holds a wall of patents that prevents competitors from copying their technology. This has already translated into high-margin licensing deals with 3M and The Siemon Company.

CRDO Financial Metrics: Revenue Growth and Gross Margin Trends

Credo has locked in all four major hyperscalers, plus SpaceX and a growing list of neo-cloud providers.

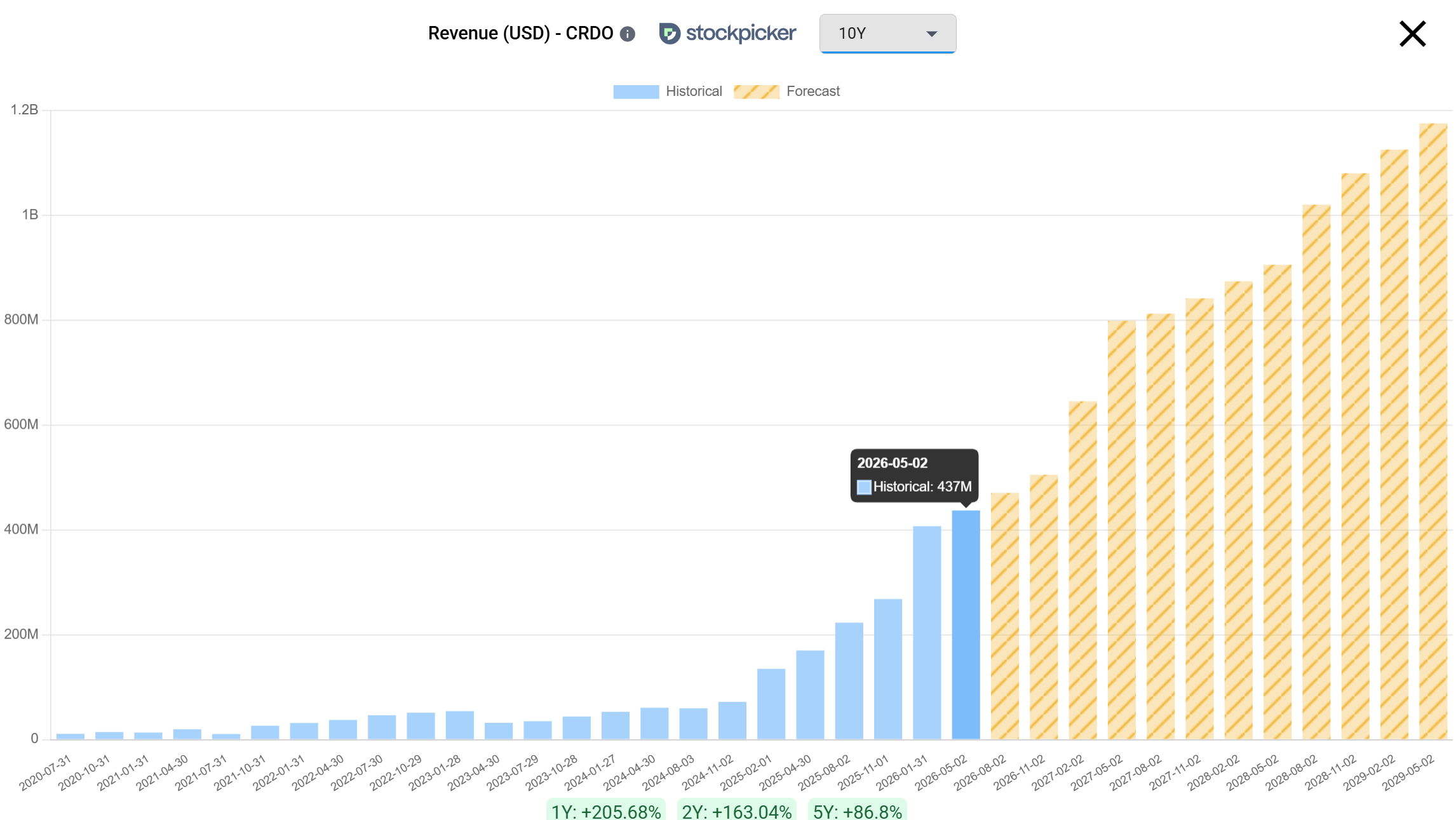

Revenue last quarter hit $437 million, up from $170 million in the same period last year. That is 157% growth year-over-year. To put that in perspective: in one quarter, they generated the same revenue they made during the entire fiscal year of 2025.

Analysts are projecting $6 billion in revenue by 2031. But Wall Street follows market sentiment, and right now sentiment around semiconductor stocks is extremely positive. Take analyst models as a direction, not a promise.

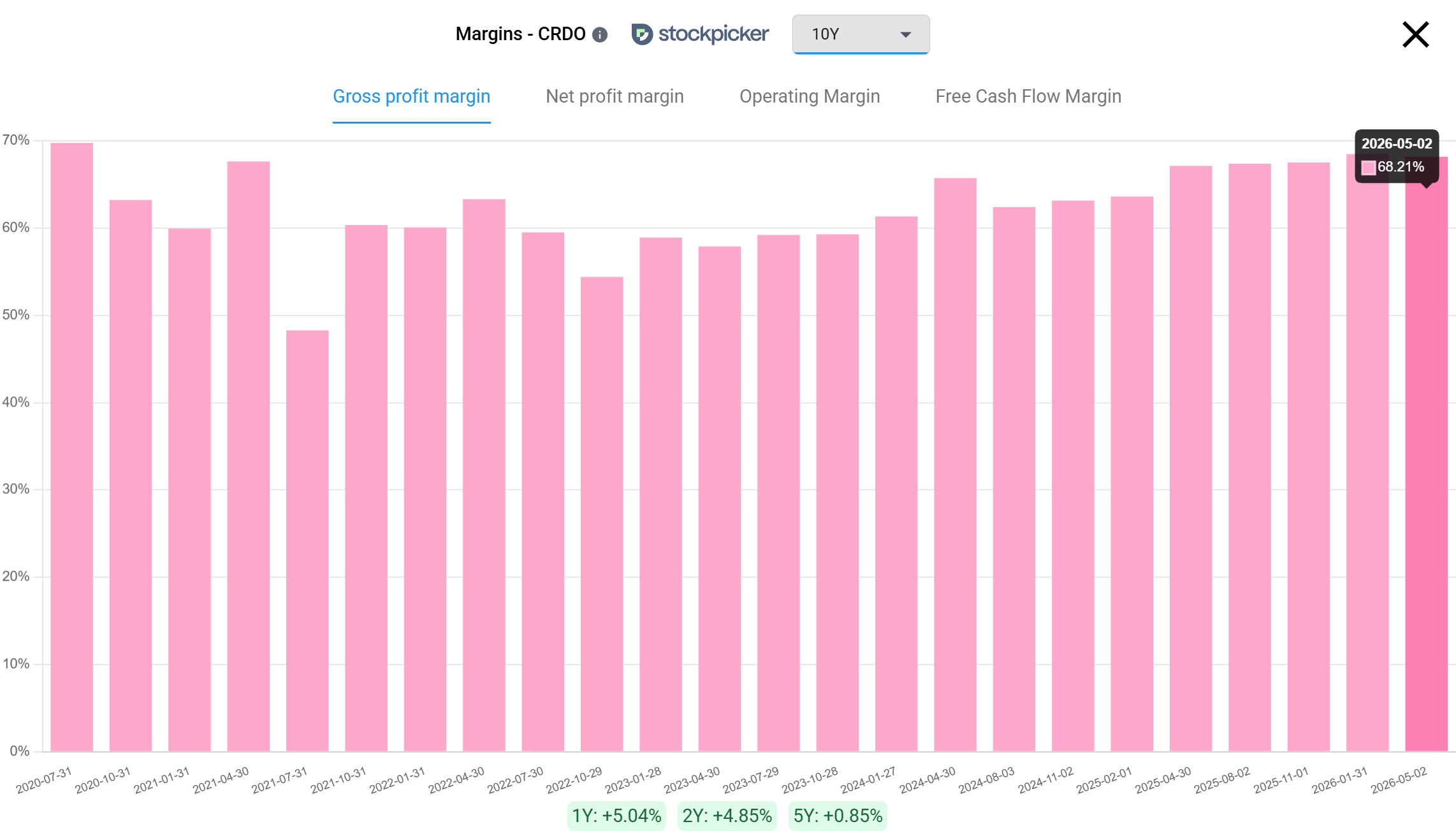

Gross margin last quarter was 68%. This is the most important number to watch. As long as it stays at this level, the competitive moat is intact. If it starts dropping, it signals that pricing power is weakening.

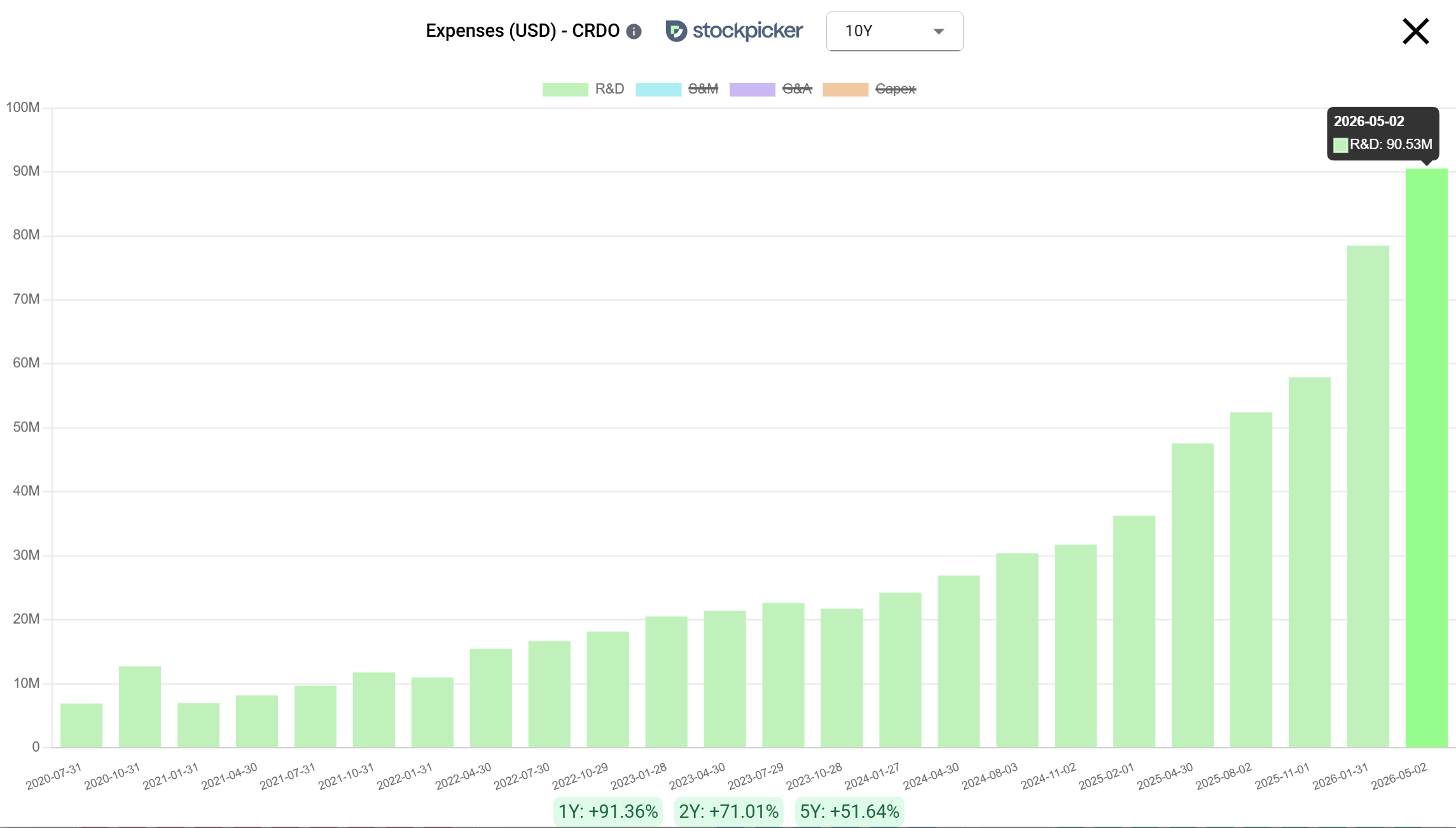

Credo is also increasing R&D spending as the industry transitions to higher connection speeds — which brings us to the biggest risk.

The 1.6T Transition Risk: Copper vs. Silicon Photonics

Think of data center cables as highways between processors. Until recently, the speed was 800 gigabits per second — eight lanes running at 112 gigabits each.

Credo's copper AEC cables were the best solution inside a single server rack and could bridge different racks up to seven meters apart. But the industry is now transitioning to 1.6 terabits per second — eight lanes running at 200 gigabits.

At this speed, copper hits a hard physical limit. Active electrical copper cables are still the best option inside a single rack. But for rack-to-rack connections longer than three meters, copper becomes obsolete at 1.6T. Optics takes over.

And optics is Marvell Technology's domain. Marvell is aggressively deploying capital there, including their acquisition of Celestial AI.

CRDO M&A Strategy: Silicon Photonics and the Dustphotonics Acquisition

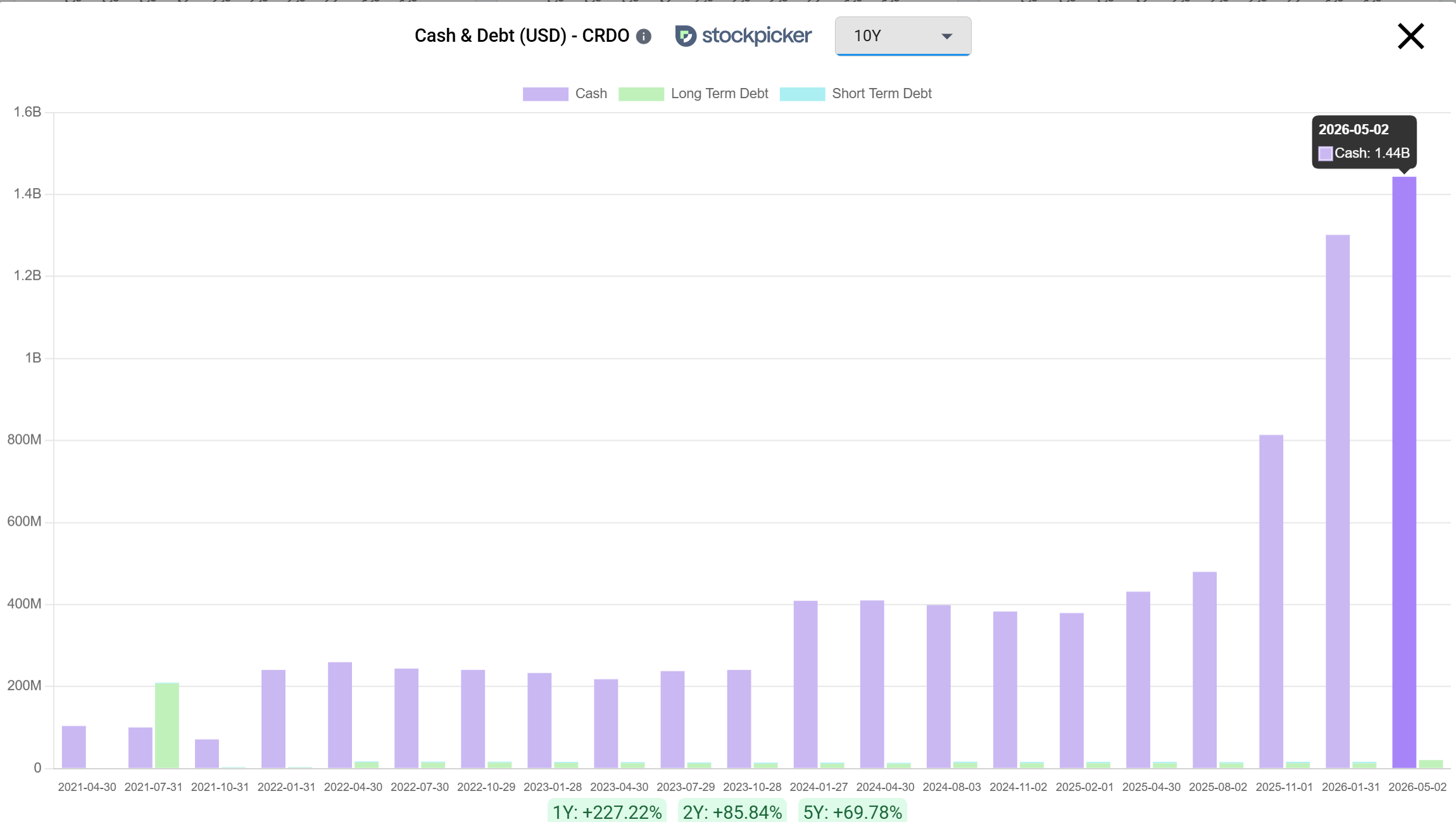

Credo is not sitting still. They have $1.4 billion in cash and are using it to acquire smaller players and force their way into silicon photonics. Their most recent acquisition is Dustphotonics — $750 million in cash plus a potential payout of 920,000 shares.

The goal is vertical integration. Credo does not need to dominate optics to survive. Hyperscalers want a third option to break up the current Marvell and Broadcom duopoly. Credo's job is to be that option.

Whether the Dustphotonics acquisition is enough to protect their margins through the transition is the core question.

CRDO Shareholder Dilution: Stock-Based Compensation & Amazon Warrants

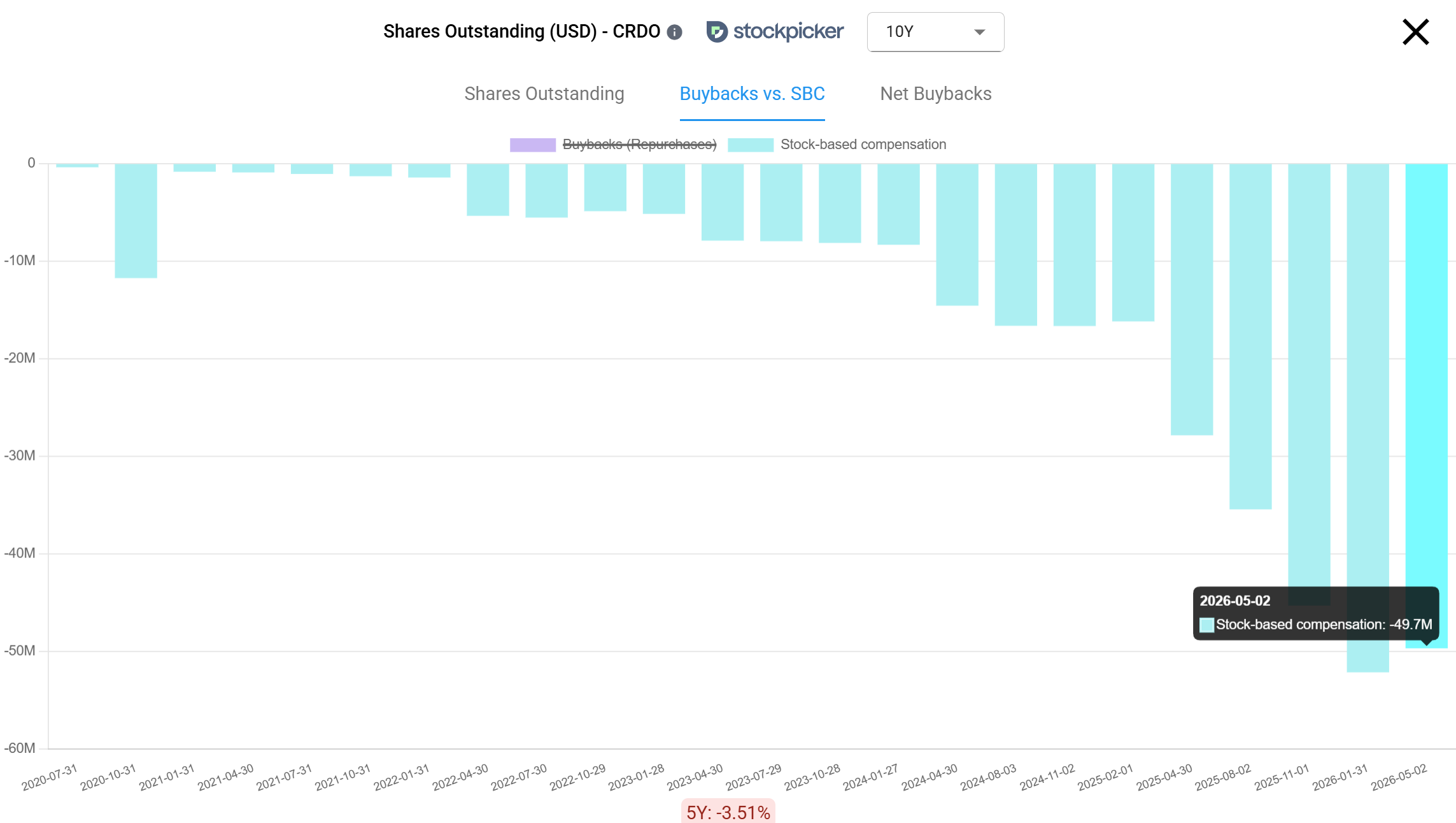

Credo is diluting shareholders through stock-based compensation, acquisitions, and corporate warrants.

Amazon had a deal allowing them to purchase 4.1 million Credo shares at $10.74 per share. Amazon hit the milestone and vested all of those shares. The Dustphotonics deal adds potential further dilution through the share component.

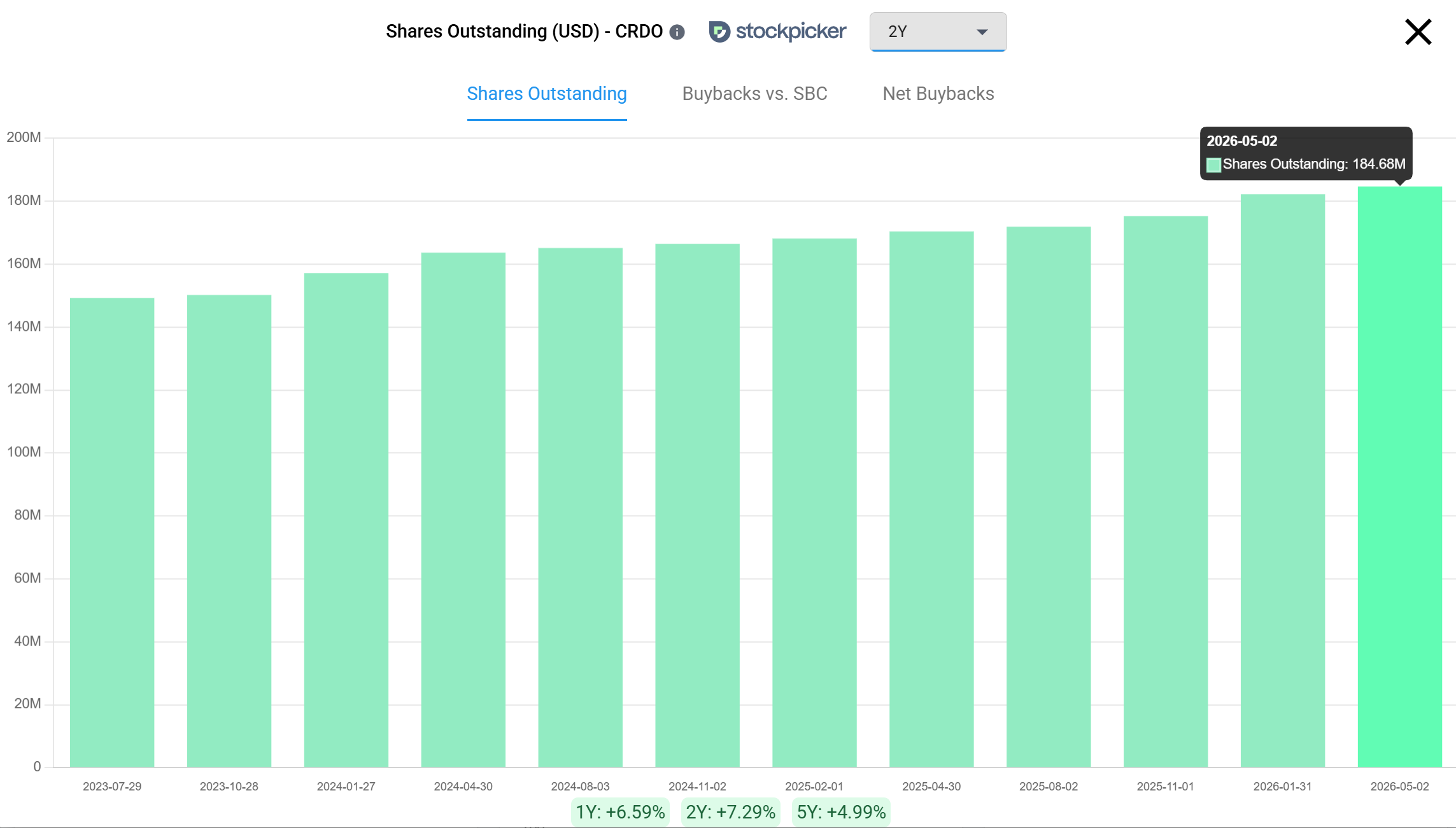

Shares outstanding grew from 163 million to 184 million over two years. That is 12% dilution in two years, and the pace will likely continue as acquisitions progress.

Is CRDO Stock Overvalued? 41x Price-to-Sales (P/S) Multiple Analysis

The stock is now priced at 41x price-to-sales. That multiple assumes growth continues at close to the current pace and that the optical transition does not materially damage margins.

Both assumptions need to hold simultaneously. And there is a concentration risk on top of it: the majority of Credo's revenue comes from a small number of hyperscalers. If one of them switches vendors or brings the technology in-house, the revenue impact would be significant.

CRDO Risk-Reward Profile: Final Takeaways

Credo is a rare example of a company where the hyper-growth is completely real. The technology is genuinely differentiated, the switching costs are real, and the customer list is as good as it gets in this industry.

But even high-quality businesses have a price where the math no longer works. At 41x sales, with a copper-to-optics transition on the horizon and 12% dilution in two years, the margin of safety is thin. The business is excellent. The entry point matters.

To analyze the visual fundamental charts, historical revenue growth, and gross margin trends for this stock, view the Credo Technology (CRDO) Financial Dashboard on Stockpicker.

Full disclosure: As of the moment of writing this article, the author does not have any exposure on CRDO stock